Boeing Stock Has Declined Significantly, But Outlook Has Not Improved (NYSE:BA)

Stephen Brashear/Getty Photos News

Investment decision thesis

The article-pandemic recovery of air vacation and international tourism demand from customers offers great earning options for companies hit really hard in 2020, and The Boeing Enterprise (NYSE:BA) is one of them. However, the broad overall economy is not the only detail to shape Boeing’s valuation. Despite the options, the firm is still not building money because of to output line stoppages and delayed shipments.

In the past write-up, we highlighted Boeing’s questionable small-phrase outlook, and our anticipations of the stock’s overall performance have been borne out. Just after the current collapse of Boeing’s Q1 2022 financials, Boeing’s rates have dropped, and, according to our calculations, the stock is now trading at its honest stages.

Boeing stock is nonetheless far from the entry point due to many variables. The primary situation is uncertainty about the 777x design, whose product sales have been moved from 2023 to 2025. It is also probable that Boeing will get started to bring in personal debt or dilute the inventory yet again mainly because of the firm’s unprofitability.

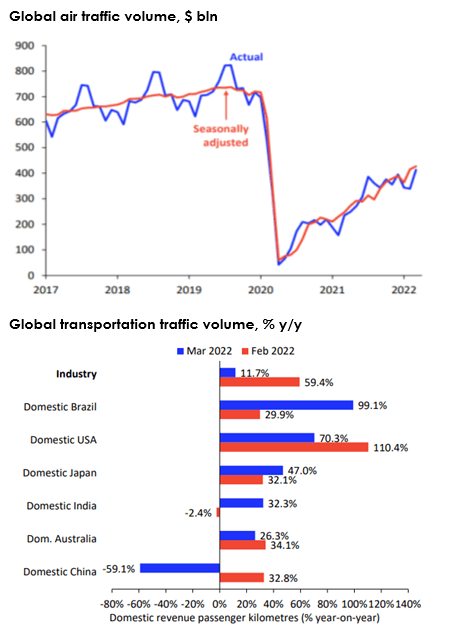

Air journey market place keeps on recovering

The air vacation market place retains its restoration to pre-pandemic levels. Even with the COVID-19 outbreak in China, which experienced a considerable effects on air journey in Q1 2022, we do not revise our outlook assuming full marketplace restoration by 2024. Boeing is a immediate beneficiary of this phenomenon – airways will improve their CapEx courses and receive aircraft into their fleets to fulfill growing demand, so as the wide airline market place grows, Boeing could significantly strengthen its effectiveness in Professional Airplanes and World wide Companies segments.

IATA

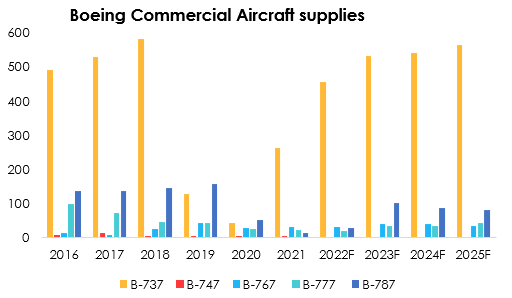

Industrial airplanes section

Business airplanes generation is the major Boeing section by revenue and continues to be challenged by regulatory actions by the FAA and delays in output of new designs. At the close of Q1, the company announced just one a lot more shift in its forecast for new design materials. Significantly, one particular of the most predicted types, the Boeing 787, whose sales have been halted in Q2 2021, is very likely to be offered for provide only in Q3 or Q4 2022. Income of the 777X product (cargo plane) have been postponed from late 2023 to early 2025 due to FAA approval, inspite of the latest prosperous testing and demonstration in the UAE.

The company’s very best-providing design, airliner Boeing 737, has a short while ago been the subject matter of extreme discussion from aircraft providers and regulators. The plane crash in China, which is continue to less than investigation, has produced uncertainties about the trustworthiness of the model supplied. Consequently, some Chinese airways have scaled back plans to acquire new Boeing types for their fleets. However, the company’s items have not fully remaining the market place even with decreased demand in China, but the epidemiological circumstance in the location also results in additional challenges. Lockdowns have disrupted the resumption of the B-737 MAX design materials to China, a offer practically agreed upon, in accordance to the management. In 2023, Boeing competitor Comac C919 may perhaps press the Boeing 737 in Asia. Nevertheless, full replacement of the 737s, enable by yourself the entry of a new airliner to wide markets, is not likely in the in the vicinity of potential.

Firm data, Calculations by Spend Heroes

Business airplanes section

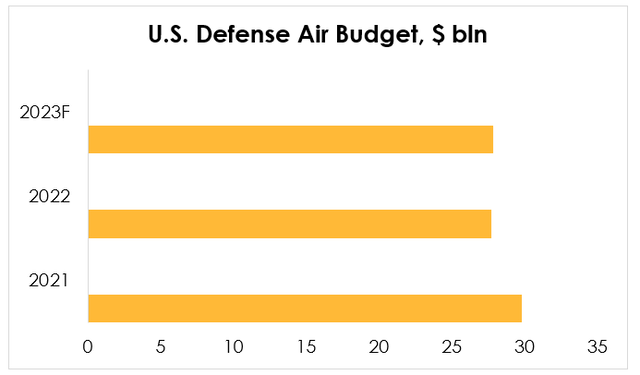

The U.S. governing administration is the key shopper of Boeing in the protection section. The corporation supplies the Department of Protection with armed service plane and performs carefully with NASA.

Despite expected raise in full U.S. protection funds, plane purchases in 2022-2023 will lessen in contrast to 2021. NASA will also not acquire major additions to its yearly spending budget, with only 3% y/y maximize in 2022 and 8% requested maximize in 2023, which could be lowered based on the government’s decision.

United states of america Department of Protection

As for each our calculations, the result of the 2022 protection finances reduction on the plane spending budget will strike Boeing’s section earnings by -9.6% y/y.

Boeing company margin

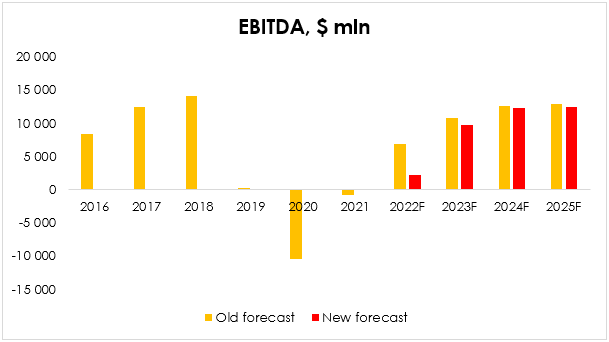

In addition to declining revenues, Boeing enterprise margin is also influencing its financial investment potential clients.

The firm’s major difficulty now is the prices induced by the shutdown of creation traces. Administration estimates about $2 bln is the irrecoverable part of the losses, mostly prompted by the freeze in B-787 production. The business hopes to create off costs by the end of 2023 – that is, about $300 mln for each quarter. Q1 margin was also negatively impacted by higher progress costs, but we do not feel this will be long-lasting thanks to the size and mother nature of Boeing’s business enterprise.

A different equally vital part is the macroeconomic component. In Q1 2022, aluminum selling prices and labor shortages ended up the most sizeable contributors to economic final results. We do not feel the impact will previous way too extended thanks to the cyclical character of the economics, but Boeing could return to historic margin levels by 2024, by the time the airline current market is totally recovered and the business auto offer chain is stabilized.

Thus, we improve our 2022 EBITDA forecast from $6,912 mln to $2,207 mln and from $10,787 mln (+56% y/y) to $9,683 mln (+340% y/y) in 2023.

Company data, Calculations by Spend Heroes

Valuation

Boeing is a beneficiary of the recovering demand from customers for airline expert services, but the firm’s inner issues similar to continuous postponements of aircraft provides and losses connected to the similar cause are presently mirrored in the industry worth.

Components that will affect the acceleration in the price of securities above the following 12 months:

- Resumption of the B-78 supplies in volumes above consensus

- Signing of major contracts for plane supplies

- Types nonetheless to produce (777X. 777-9) approval faster than industry expectations.

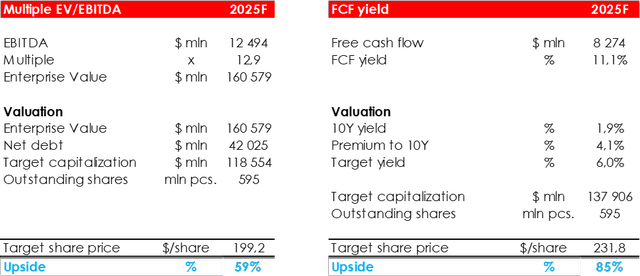

We estimate our concentrate on price tag for Boeing stock at $154 for each share and believe that the marketplace is now relatively valuing the firm from a essential situation. Hold rating, upside – 23%.

Pitfalls

- Improve in Boeing aircraft mishaps, which would impact need for Boeing aircraft and develop more issues with regulatory authorities and

- It is also doable that Boeing will begin to draw in credit card debt or dilute the inventory all over again since of the company’s unprofitability.